As a common business language for the financial marketplace, ISO 20022 is firmly positioned as a unifier for new and contrasting FinTech innovations, such as Distributed Ledger Technology (DLT), Smart Contract (SC), and Application Programming Interfaces

(APIs).

Considered the de facto, universal business language for financial industry initiatives, ISO 20022 acts as an enabler for new and emerging innovations.

One could imagine rich data mining solutions responding to regulatory requirements because all business segments could be aligned across different systems within an organization. Similarly, such business alignment would make it easier to create universal

web and mobile payments or machine learning solutions – all thanks to a robust fundament of aligned business flows. Equally, adopting the prevalent financial services business-standard would contribute to the seamless deployment of a FinTech solution since

most of these solutions have a complementary role.

Value of ISO 20022 for FinTech The value provided by ISO 20022 across different FinTech implementations can be summarised in four areas:

Open and collaborative standard:

A key enabler for the future of open banking. Any organization can make use of standards and design messages in a collaborative way as open standards are not controlled by a single commercial interest, and are publicly available.

Tech-neutral business language:

ISO 20022 provides the means to achieve a uniform and unambiguous interpretation of the data exchanged among users, regardless of different technologies in use within and across the financial industry. Based on universal business models, the common standards

can be enhanced to incorporate features of new technology and can be made tangible by adopting a physical standard. For this reason, ISO 20022 does not necessarily have to be expressed in XML messages and could, for example, also be rendered in JSON.

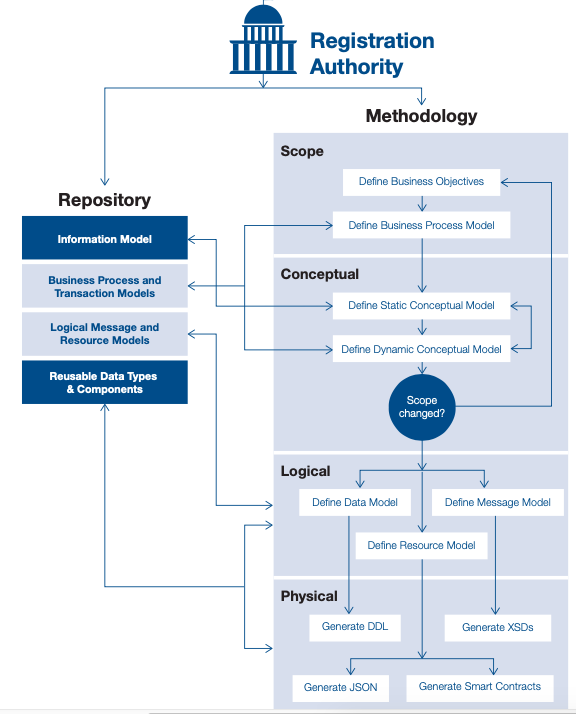

Rich and proven data model:

Allows any user to create ISO 20022 messages and data structures including new contents in the business model to define the financial business concepts, processes, flows, and inter-relations. The ISO 20022 repository contains reusable concepts and data components

that could be reused to create a business data record in a distributed ledger.

Global interoperability:

ISO 20022 facilitates interoperability at three levels; business, syntax, and semantics. Business interoperability enables organizations to seamlessly execute business goals and objectives. Syntax interoperability aligns the exchange of data between different

applications in the right protocols and valid formats, while semantics interoperability ensures the consistent meaning of the information.

Image source - SWIFT

Examples of ISO 20022 for unifying FinTech

New Payments Platform (NPP), Australia : Design, and definition of common data structures to support interactive addressing service dialogues that enable resolution of beneficiary account identification through mobile numbers and email addresses.

Status: The NPP central infrastructure is live as of 2017.

Australian Securities Exchange (ASX): ISO 20022 standards could facilitate interoperability between the messaging layers and dataset in a potential DLT service for Post Trade Services. It could also drive interoperability and alignment with other

Australian market infrastructures like NPP who have adopted ISO 20022.

Status - Expected Go-Live - 2021

DLT and Smart Contracts for bonds: ISO 20022 business model and content are applied to automate the securities transaction lifecycle of bonds including auto-coupon payments to achieve interoperability between DLT/ SC platforms and other automation

mechanisms.

Status: Proof of Concept (POC).

DLT and APIs for Nostro account reconciliation: The business data set used for DLT and APIs are based on ISO 20022 to ensure data consistency between the ledger content and APIs and interoperability with banks’ ledgers. This facilitates the monitoring

and management of intraday liquidity for efficient cross-border payments.

Status: POC.

APIs for SEPA Instant Payments: The payment data set used to exchange information between third-party payment providers and account servicers by APIs and is based on ISO 20022 which would comply with the new European Payment Services Directive – PSD2.

Status: Prototype.

SWIFT gpi: The components used to define the API calls for payment status and tracking in gpi will be ISO 20022 enabled, it will foster mapping with the corresponding ISO 20022 messages for which these API calls were defined and are operated.

Status: Production.

ISO 20022 is not a IT change or a compliance exercise. It is a journey into the future of financial services.